Will Uber Ever Get Where It’s Going?

Will Uber Ever Get Where It’s Going?

And if it does, how will we rate the ride?

Dear Reader,

Let me preface today’s newsletter by making clear that none of what follows is investment advice.

I’m not licensed to give investment advice. I’m also not qualified to. I’ve built valuation models, but only ever while keeping a graduate of the Sloan School of Business within arm’s reach at all times. I’m not even interested in giving investment advice – I’ve never owned a single share of stock in my life.

What follows is strategic analysis, some of it informed by math, most of it simply informed by logic. For the most part, I’m just asking questions. To the extent that I will offer hypotheses or opinions, it should go without saying that I could be wrong (this is true of my newsletter more broadly, of course).

Even if I’m right, it could all be baked into the current stock price – in fact, if we believe in efficient markets, we should assume that it is.

For what it’s worth, according to NASDAQ the analyst consensus is that Uber is a strong buy - 33 major analysts give it such a rating, with an average price target of $48 compared to a current stock price of $31.

I’m not at all invested – literally or metaphorically – in what happens to Uber’s share price. But I am interested in Uber as a business, and that’s what today’s edition of the newsletter is about.

Note: there are a lot of charts and images in this post so it may be truncated in your email inbox. If you see something saying “View Entire Message”, click on it. Alternatively, visit the site.

Uber’s strategy in a nutshell

If you read Uber’s Investor Day 2022 presentation, they lay out their strategy quite clearly.

They’ve expanded their product offering in mobility…

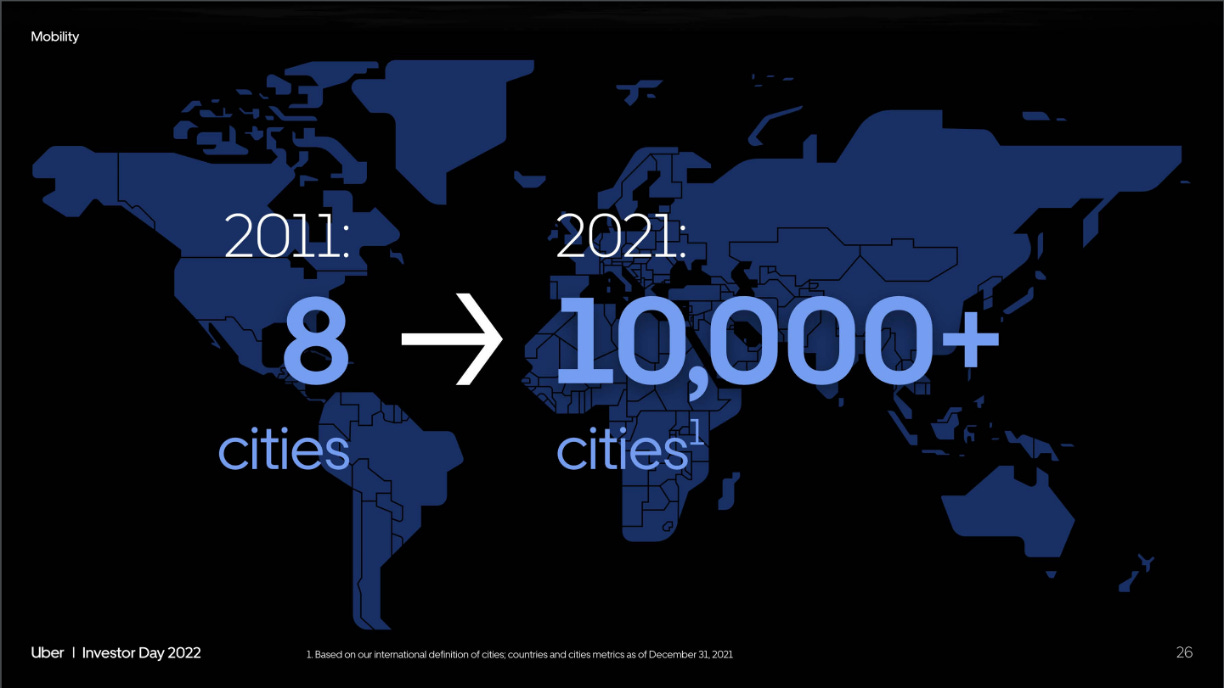

…and they’ve expanded their geographic footprint…

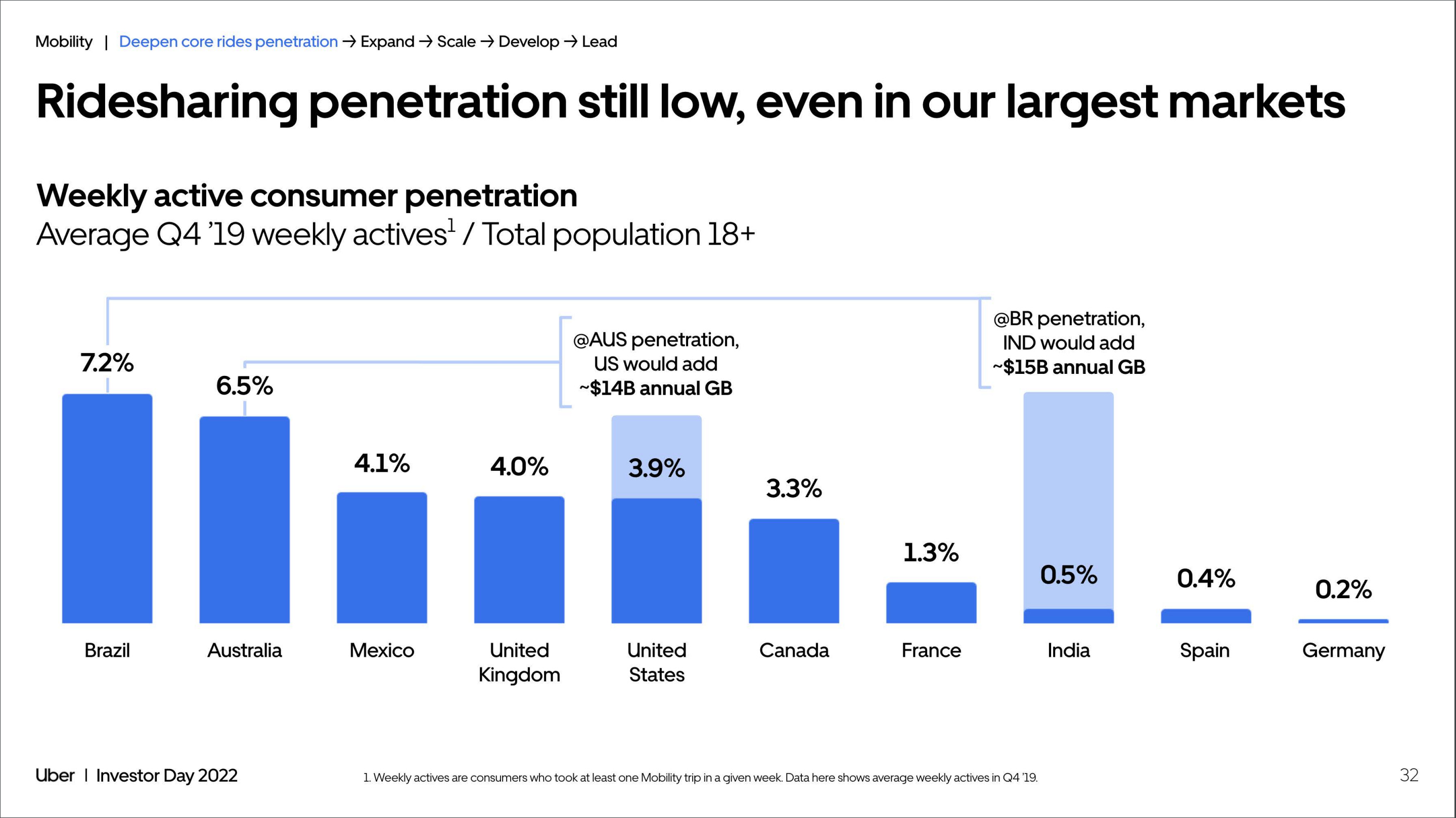

… all of these markets are under-penetrated…

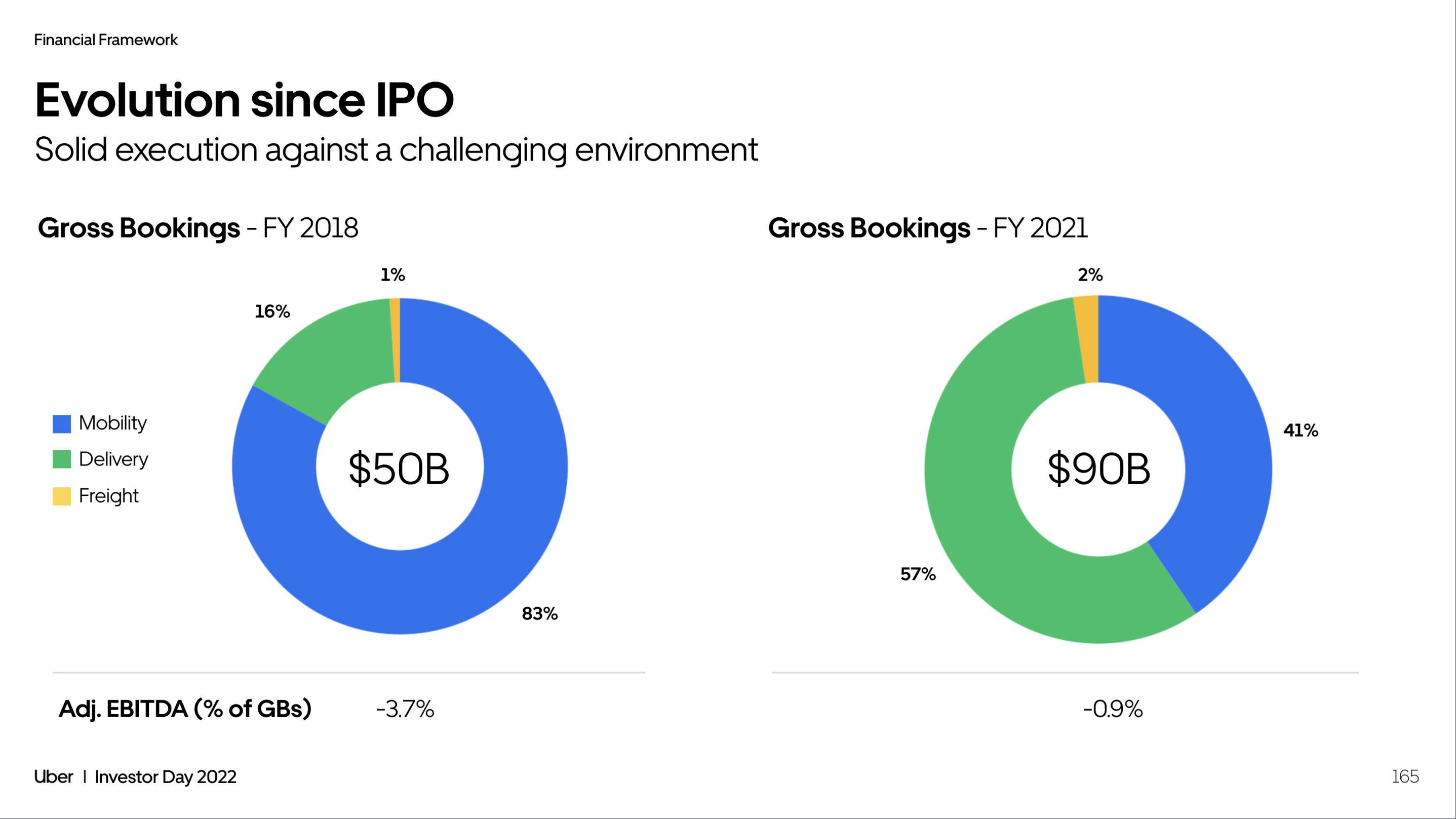

… and they’re not just a mobility business these days anyway…

… so if they keep growing and manage their costs, they’ll be profitable:

In a nutshell: virtually limitless growth horizons plus a path to profitability equals potential for massive value creation. What’s not to like?

Clearly, the analysts buy it and I’m not saying I don’t. I’m just wondering whether it will be quite as easy as they are trying to make it look.

Uber’s core business model was a win-win-win

It’s worth remembering that at the heart of Uber’s business model is a very clever idea.

Pre-Uber, limo drivers had to build up their own client list or work for a limo company, or some combination of the two. Either would provide them with a base load of clients that covered the cost of the car and allowed them to make a living.

But there is a lot of waiting around involved in driving a limo – there are only so many people who can afford to reserve a car at a high hourly rate and you can only schedule so many of those jobs in a day.

This was the original insight at the core of Uber and it was brilliant: what if we could connect price-sensitive customers on a short-notice basis to idle limo drivers?

The phrases “price-sensitive” and “short-notice” are important because the core limo customer is not price sensitive at all. They pay a premium to know that a car will be ready when they are. Uber appeals to a more price-sensitive consumer because it offers a cheap ride to those willing to take the risk that a car won’t be available when they need it. By tapping into price-sensitive customers, Uber was not cannibalizing the limo driver’s core business.

The phrase “idle limo drivers” is important too because the economics of an idle driver are very different from the economics of driving in general.

Let me illustrate this with some very rough math. It’s so rough I’m not even going to use numbers, but I have discussed this with enough folks in the industry over the years to know that this picture is directionally, conceptually, illustratively right. I’ll walk you through this chart with some narration below.

The height of the bar is the hourly rate charged for the ride and the segments show where the money goes.

Column A illustrates the hourly economics of the average limo job. The average job has to bear some of the burden of the fixed costs of the limo driver, like the cost of the car and insurance, as well as all of the variable costs associated with that ride – gas, tolls, parking etc. What’s left over is the driver’s income.

Column B illustrates the hourly economics of an incremental ride if the driver was able to secure it themselves and charge their usual hourly rate. The fixed costs are already paid for by the other jobs you’ve booked that day so, as you can see, that one extra ride is very lucrative to the driver.

But it’s illegal for a limo to solicit rides on the street, so how does the driver find that incremental ride?

Enter Uber.

Column C illustrates the power of the original model – even with a lower fare and even after Uber takes a cut, the driver still makes money, because on these incremental rides they only have to cover their variable costs.

It’s less than the driver would have made had they been able to source that additional ride by themselves but, since it was largely beyond their ability to source that incremental ride, this is as good as found money.

Uber could replicate this model in any large metro market that had an already established fleet of limos – the existing limo companies and drivers have built up a business that makes them a living, and now Uber can bring drivers incremental trips that are very profitable.

Major markets, established limo drivers, incremental customers, incremental economics. A win for customers (cheaper rides), a win for drivers (incremental income) and a win for Uber. Brilliant.

Had Uber stuck to this model it would have been a very successful, very profitable, albeit much smaller, business.

Keep reading with a 7-day free trial

Subscribe to The Armchair Strategist to keep reading this post and get 7 days of free access to the full post archives.